Paying for Educational Expenses TAX FREE – Comparison of the Coverdell and 529 Plans

Posted on September 7, 2020

With the new school season just around the corner, you have probably already started working on your school’s supplies lists. However, the beginning of the year isn't just the only time you spend money for school. Materials for projects, electronics for homework, maybe even school uniforms and tuition are things that come at all times during the school season. Wouldn't it be nice if the money used for education costs were exempt from federal income taxes? They can be, and there are investment plans that allow you to do this!

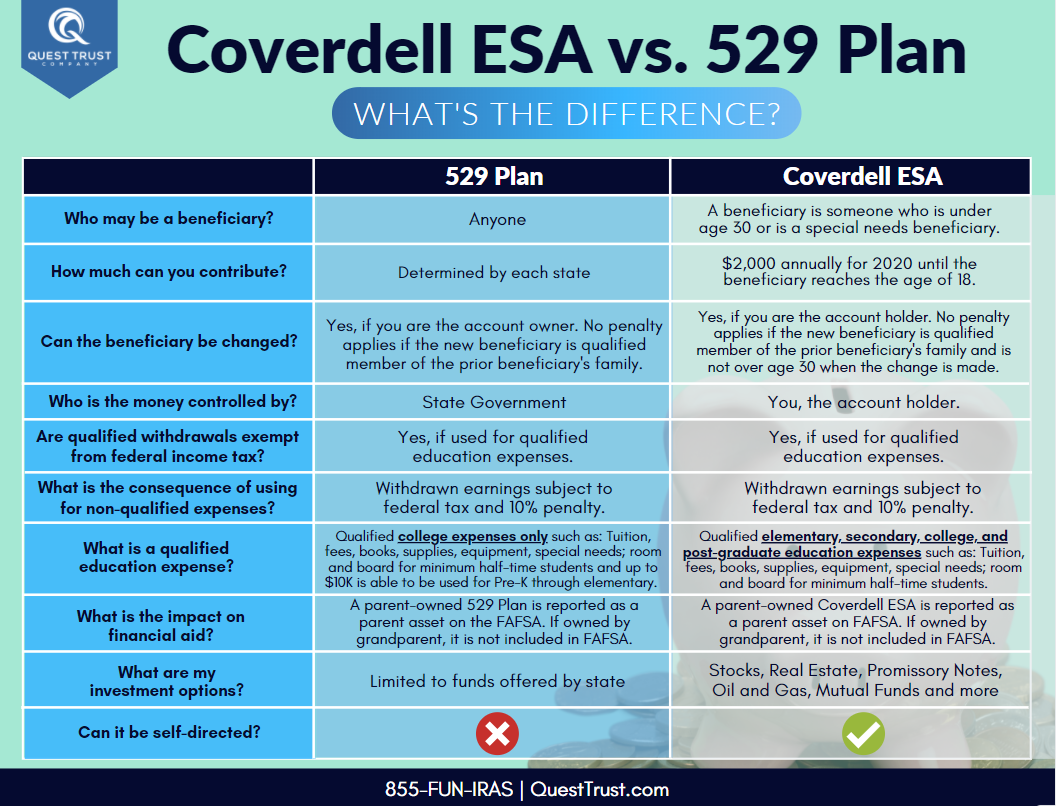

The Coverdell Education Savings Account (ESA) and 529 are similar education savings plans that allow you to save for college and other educational purposes, but their differences can determine which one is best for you. Some plans, like the Coverdell ESA, allow you to diversify your investment portfolio by investing in alternative assets, such as self-directed real estate or notes.

In this article, we'll cover the main differences and similarities so that you can get a feel for which account may best fit your needs.

The Coverdell and the 529 are both used for education, and this is the most common similarity. What does education cover? The good news is… that answer is very broad. For a Coverdell, educational expenses can cover everything from school supplies like binders and notebooks, to textbooks and even computers if the school program requires it for the class! For a complete list of qualified education expenses, please view IRS Publication 970.

Another important similarity these two accounts share are the tax benefits. For the Coverdell and 529, taxes grow tax-deferred until distribution. If used for qualified educational expenses, these plans offer tax-free growth! It's important to note that non-qualified expenses that are withdrawn could be subject to federal taxes and a 10% penalty tax.

What can you use these accounts for?

Their differences are where the two accounts are set apart. Though they are both great accounts that can be used for education, one account allows you to begin using it earlier than the other. The Coverdell ESA funds can be used for qualified expenses from Pre-K all the way up to college, whereas the 529 plan funds can be used for qualified college expenses, but has a $10,000 limit if you are using it to cover K-12 expenses. This is something to consider if the funds were needed for secondary school tuition.

What are the contribution limits?

Another difference is the contribution limits. With a 529 plan, the limit varies by state, whereas the Coverdell ESA remains the same across the board (for 2023 the annual contribution limit is $2,000 per child, per year until the child reaches age 18).

One unique characteristic of the Coverdell ESA is that even though contributions must stop at age 18 (the age of majority), the account can remain in that child's name until age 30 or it can be passed along to another eligible family member. (Special needs beneficiaries are not affected by the age restrictions.)

In order to contribute to a Coverdell ESA, the adjusted gross income of the depositor must be less than $110,000 if single, or $220,000 if married and with a 529, there are no income limitations.

It is important to note that gift contributions can be made to a Coverdell. This means that if a contributor's income level was higher than the limit, another person could contribute to his or her place. For example, if a child's parents made too much, but had grandparents who were under the income limit, they would be able to contribute to the Coverdell if they wanted.

What can you invest in?

The biggest difference is who is in control of the investments. With a Coverdell ESA, the account holder has the option to choose his or her own investment. If you want even more flexibility, you can open a self-directed Coverdell ESA which gives you the option to purchase alternative investments. One investment strategy is to partner the child's Coverdell account with their parents' self-directed IRAs to purchase real estate investments and even private loan partnerships. Deciding whether you want to take control of the account or let the state make the investment decisions will be important when picking which education account is best for you.

Coverdell ESA and 529 are both beneficial accounts to have for school savings and qualified educational expenses. However, both come with their own freedoms and restrictions. It's up to you to decide how much control you want to have over the account and how you anticipate your future spendings. When in doubt, consult with a tax advisor to make sure you are accounting for the expenses properly.

If you would like more information about the Coverdell ESA or have questions about which plan might be right for you, you can speak with an IRA specialist at 855-FUN-IRAS (855-386-4727). To learn more about how to get started investing with a self-directed ESA, schedule a 1-on-1 consultation with an IRA Specialist by clicking HERE.

share this article

Related News & Articles

View All chevron_right July 12, 2023

Top 10 Things You Need to Know When Investing in Real Estate Notes with Your IRA

Learn the common mistakes new investors make when lending their money from their IRA.

July 12, 2023

Top 10 Things You Need to Know When Investing in Real Estate Notes with Your IRA

Learn the common mistakes new investors make when lending their money from their IRA.

March 23, 2023

Active vs. Passive Note Investing - Which is Right for You?

Guest author Fred Moskowitz, note investor and best-selling author, compares active and passive note investing.

March 23, 2023

Active vs. Passive Note Investing - Which is Right for You?

Guest author Fred Moskowitz, note investor and best-selling author, compares active and passive note investing.

June 01, 2022

Hard Money Loans Made Easy

Guest article by Investor Loan Source

June 01, 2022

Hard Money Loans Made Easy

Guest article by Investor Loan Source

March 28, 2022

Self-Directed IRAs and Seller Financing

Quest is joined by Eddie Speed, founder of NoteSchool, to give a basic overview of seller financing with your SDIRA.

March 28, 2022

Self-Directed IRAs and Seller Financing

Quest is joined by Eddie Speed, founder of NoteSchool, to give a basic overview of seller financing with your SDIRA.