Get our e-newsletter for all the exciting updates, events notices and valuable education

IRS Announces Contribution Limits for 2024

Understand the current IRS contribution limits so you can maximize your savings.

Posted on November 8, 2023 by Rebecca Parker

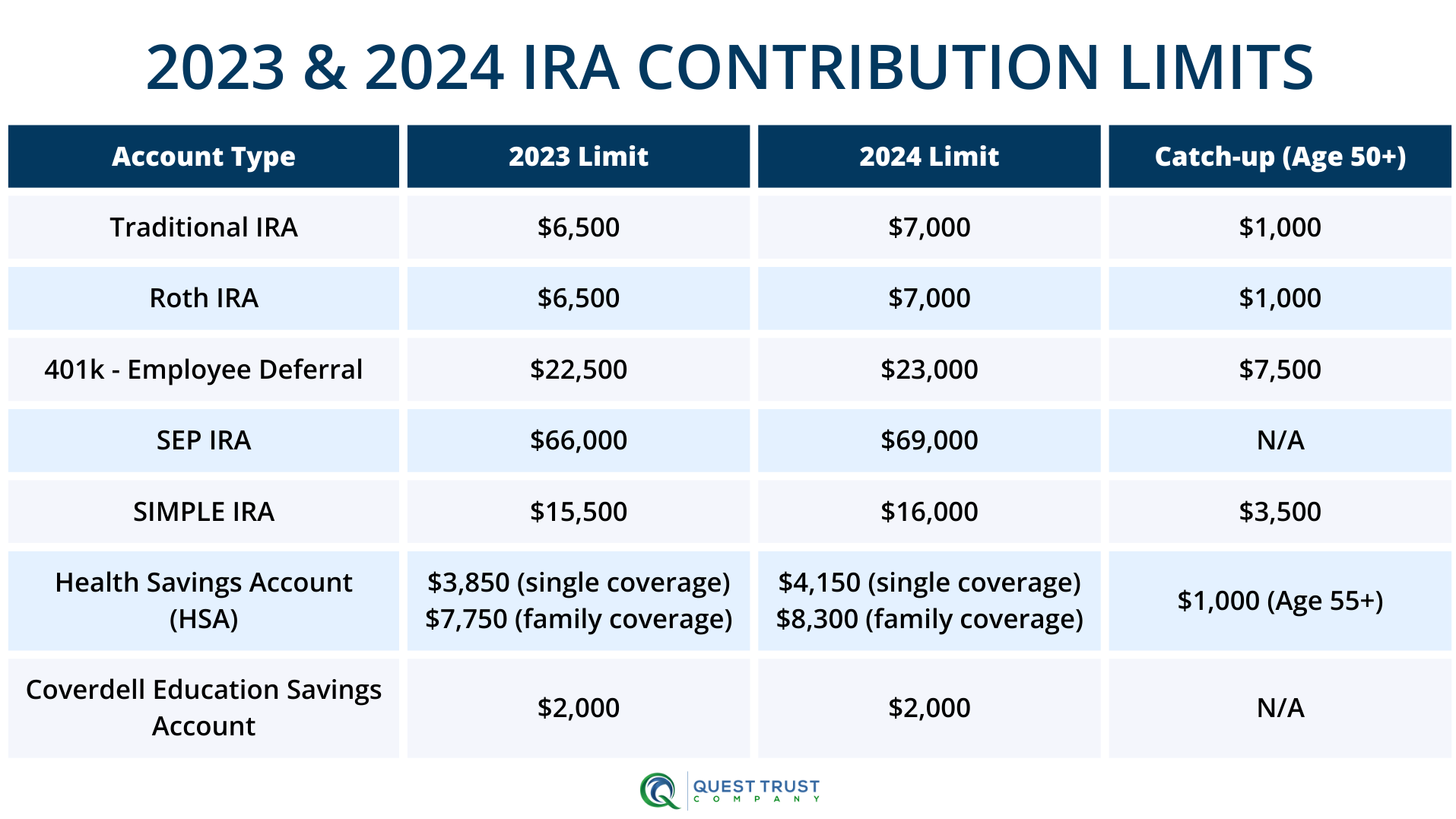

As the year draws to a close and Americans eagerly wait for the holiday season to begin, those of us in the retirement industry wait with great anticipation for the IRS announcement of the upcoming year’s contribution limits. That time has arrived, and Quest is here to summarize the changes. Most plans received a cost-of-living increase for contributions this year, with catch-up contributions for those 50 and over (55 and over for HSAs) remaining the same as last year. Here is a review of the changes so you can start planning your 2024 contributions.

Traditional and Roth IRAs

Two of the most popular accounts, Traditional and Roth IRAs, saw a $500 increase bumping up their contribution limits to $7,000 from $6,500 in 2023. Catch-up contributions will remain the same at $1,000, so for age 50 and over, you can contribute up to $8,000. It’s important to note that contribution limits for Traditional and Roth IRAs are for the combined total, so you can contribute up to $7,000 total between the accounts, not to each account.

For taxpayers that are eligible to deduct contributions to their Traditional IRA, those phase-out ranges have been increased as well. There are several factors that make up the phase-out limits for the tax deduction, including if you are covered by a plan at work and if you are filing single or married. For an explanation of those limits, please refer to the full article on the IRS website.

Roth IRA Phase-Out Ranges Increase

Roth IRAs will also see an increase in their phase-out ranges, allowing more individuals to be able to contribute to a Roth in 2024. Phase-out ranges dictate if you will be able to make a full contribution, a partial contribution, or any contribution at all to a Roth account for the current year, and these limits are based on your Modified Adjusted Gross Income (MAGI).

For single and heads of households, the Roth phase-out range has been increased to between $146,000 and $161,000, which means if you make less than $146,000, you can make a full contribution to your Roth and if you make between $146,000 to $161,000 you can still make a partial contribution. Single filers will not be able to make any contribution once they are over $161,000.

For married couples filing jointly, the phase-out range has been increased to between $230,000 to $240,000, allowing couples to contribute at least a portion of their income to their individual Roth IRAs as long as their combined income is under $240,000. This is an increase from 2023 where the phase-out range was $218,000 and $228,000. For a married individual filing a separate return, the phase-out range is unchanged.

Employer Plans

Employer plans will receive an increase in contribution limits as well. The SIMPLE IRA (Savings Incentive Match Plan for Employees) will receive a $500 increase on employee contributions from $15,500 in 2023 to $16,000 in 2024. The catch-up contribution remains at $3,500, allowing those 50 and over to contribute a maximum of $19,500 into their account.

The SEP IRA (Simplified Employee Pension) will also see a contribution increase in 2024 growing from $66,000 to $69,000. SEP plans work a little differently, since only employer contributions are allowed and the amount a company contributes is a percentage of earned income, but contributions will be capped at $69,000.

The IRS is also increasing contributions to 401k plans in 2024. Employee contributions for 401k, 403b, solo plans, and most 457 plans are increasing from $22,500 in 2023 to $23,000 in 2024, with catch-up contributions remaining steady at $7,500.

Health Savings Accounts (HSA)

HSA’s will get a big boost in 2024, with single plan contribution limits increasing to $4,150, which is a $300 increase from 2023. Family HSA plans will jump to $8,300, which is a $550 increase from 2023. Catch-up contributions are available for either plan and will remain at $1,000 for those 55 and over.

Coverdell Education Savings Account (ESA)

While the Coverdell is not a retirement plan, it is a plan that Quest offers. The IRS has not announced any changes to the contribution limits for ESAs, but the limit has remained consistent at $2000 per child per year since 2002, so no change is expected at this time.

Planning for retirement is easier if you have the latest information. We hope this helps you budget your contributions for the new year, and if you ever have questions about how to make a contribution to your self-directed IRA at Quest, call us at 855-FUN-IRAs or schedule a free consultation with an IRA Specialist.

share this article

Related News & Articles

View All chevron_right July 10, 2024

7 Questions to Ask Yourself Before Choosing Your Next IRA Investment

Ready to invest your retirement funds? Have you asked yourself these important questions?

July 10, 2024

7 Questions to Ask Yourself Before Choosing Your Next IRA Investment

Ready to invest your retirement funds? Have you asked yourself these important questions?

May 31, 2024

Top 3 Reasons to Attend Quest Expo

Hear why you don't want to miss this year's Quest Expo June 27-29, 2024 at the Irving Convention Center near Dallas, Texas.

May 31, 2024

Top 3 Reasons to Attend Quest Expo

Hear why you don't want to miss this year's Quest Expo June 27-29, 2024 at the Irving Convention Center near Dallas, Texas.

May 09, 2024

Investment Options: Getting the Most Out of Your IRA

If you are new to self-directed accounts or are looking for ideas of your investment options, this is the article for you.

May 09, 2024

Investment Options: Getting the Most Out of Your IRA

If you are new to self-directed accounts or are looking for ideas of your investment options, this is the article for you.

May 06, 2024

After Opening an Account, What's the Next Step?

Learn about the ways to fund your account and get started investing.

May 06, 2024

After Opening an Account, What's the Next Step?

Learn about the ways to fund your account and get started investing.